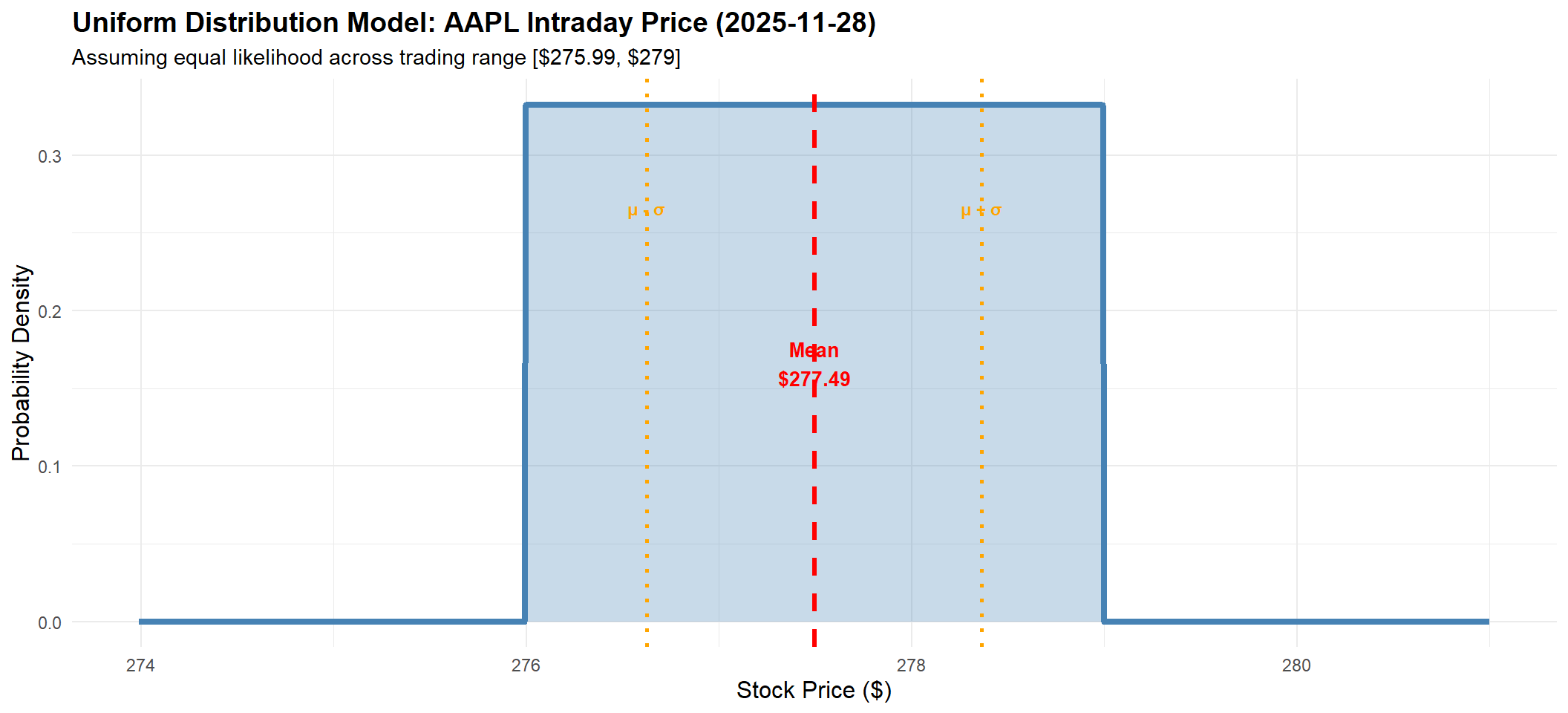

pdf_height2 = 1 / (b_unif - a_unif)

uniform_pdf_data2 = [

{x: a_unif - 5, y: 0},

{x: a_unif, y: 0},

{x: a_unif, y: pdf_height2},

{x: b_unif, y: pdf_height2},

{x: b_unif, y: 0},

{x: b_unif + 5, y: 0}

]

// Create shaded area data

shaded_area2 = d3.range(a_unif, b_unif + 0.01, (b_unif - a_unif) / 100).map(x => ({

x: x,

y: pdf_height2

}))

// Markers for mean and standard deviations

markers2 = [

{x: mean_unif, y: pdf_height2 / 2, label: "μ", color: "red"},

{x: mean_unif - sd_unif, y: pdf_height2 * 0.7, label: "μ - σ", color: "orange"},

{x: mean_unif + sd_unif, y: pdf_height2 * 0.7, label: "μ + σ", color: "orange"}

]

Plot.plot({

width: 800,

height: 450,

marginLeft: 60,

x: {

label: "Y",

grid: true

},

y: {

label: "Density f(y)",

domain: [0, pdf_height2 * 1.3]

},

marks: [

Plot.areaY(shaded_area2, {x: "x", y: "y", fill: "steelblue", opacity: 0.3}),

Plot.line(uniform_pdf_data2, {x: "x", y: "y", stroke: "steelblue", strokeWidth: 3}),

Plot.ruleX([mean_unif], {stroke: "red", strokeWidth: 2, strokeDasharray: "5,3"}),

Plot.ruleX([mean_unif - sd_unif, mean_unif + sd_unif], {stroke: "orange", strokeWidth: 1.5, strokeDasharray: "3,3"}),

Plot.dot(markers2, {x: "x", y: "y", fill: "color", r: 6, stroke: "white", strokeWidth: 2}),

Plot.text(markers2, {x: "x", y: "y", text: "label", dy: -12, fontSize: 14, fontWeight: "bold"}),

Plot.ruleY([0])

],

caption: html`<span style="color: red;">━━</span> Mean | <span style="color: orange;">━ ━</span> ± 1 Standard Deviation`

})