Mathematical Statistics

Expected Values, Covariance, and Correlation

Samir Orujov, PhD

ADA University, School of Business

Information Communication Technologies Agency, Statistics Unit

2026-02-22

🎯 Learning Objectives

By the end of this lecture, you will be able to:

Compute expected values of functions of bivariate random variables using Definition 5.9

Apply linearity properties (Theorems 5.6-5.8) to simplify expected value calculations

Calculate covariance using both the definition and computational formula (Theorem 5.10)

Compute and interpret the correlation coefficient as a standardized measure of linear association

Apply the portfolio variance formula to analyze risk in multi-asset portfolios using real financial data

📱 Attendance Check-in

📋 Overview

📚 Topics Covered Today

Expected Value of Functions – Definition 5.9 and computing \(E[g(Y_1, Y_2)]\)

Theorems on Expected Values – Linearity and fundamental result \(E[Y_1 + Y_2] = E[Y_1] + E[Y_2]\)

Covariance – Definition, interpretation, computational formula

Correlation Coefficient – Standardized covariance and properties

Case Study – Portfolio optimization with real data

📖 Motivation: Why Covariance and Correlation?

🎯 Measuring Relationships Between Variables

Understanding how two variables move together is fundamental in many applications:

Finance Applications:

- Do stock and bond returns move together or oppositely?

- How much does adding an asset reduce portfolio risk?

- What’s the systematic risk of an asset (beta)?

Other Applications:

- Does studying more hours improve exam scores?

- Are height and weight related?

- How does advertising spending relate to sales?

Key Question: How do we quantify the strength and direction of the linear relationship between two random variables?

📖 Definition: Expected Value of a Function

📝 Definition 5.9: Expected Value of \(g(Y_1, Y_2)\)

Let \(g(Y_1, Y_2)\) be a function of random variables \(Y_1\) and \(Y_2\).

Discrete Case: \[E[g(Y_1, Y_2)] = \sum_{y_1} \sum_{y_2} g(y_1, y_2) \cdot p(y_1, y_2)\]

Continuous Case: \[E[g(Y_1, Y_2)] = \int_{-\infty}^{\infty} \int_{-\infty}^{\infty} g(y_1, y_2) \cdot f(y_1, y_2) \, dy_1 \, dy_2\]

Key Insight: We can find the expected value of any function of \((Y_1, Y_2)\) by weighting function values by probabilities (discrete) or densities (continuous).

📌 Example 1: Computing \(E[Y_1 \cdot Y_2]\)

Problem: Let \(f(y_1, y_2) = 2y_1\) for \(0 < y_1 < 1\) and \(0 < y_2 < 1\). Find \(E[Y_1 \cdot Y_2]\).

Solution: Using Definition 5.9 with \(g(y_1, y_2) = y_1 \cdot y_2\):

\[E[Y_1 Y_2] = \int_0^1 \int_0^1 y_1 y_2 \cdot 2y_1 \, dy_1 \, dy_2\]

\[= \int_0^1 \int_0^1 2y_1^2 y_2 \, dy_1 \, dy_2 = \int_0^1 2y_2 \left[ \frac{y_1^3}{3} \right]_0^1 dy_2\]

\[= \int_0^1 \frac{2y_2}{3} \, dy_2 = \frac{2}{3} \left[ \frac{y_2^2}{2} \right]_0^1 = \frac{2}{3} \cdot \frac{1}{2} = \boxed{\frac{1}{3}}\]

Financial Context: If \(Y_1\) represents one asset’s return and \(Y_2\) another’s, \(E[Y_1 Y_2]\) is crucial for portfolio variance calculations.

📌 Example 2: Computing \(E[Y_1]\) from Joint Density

Problem: Using the same joint density \(f(y_1, y_2) = 2y_1\) on \([0,1] \times [0,1]\), find \(E[Y_1]\).

Method 1: Using marginal density

From Lecture 1: \(f_1(y_1) = \int_0^1 2y_1 \, dy_2 = 2y_1\)

\[E[Y_1] = \int_0^1 y_1 \cdot 2y_1 \, dy_1 = 2 \int_0^1 y_1^2 \, dy_1 = 2 \cdot \frac{1}{3} = \boxed{\frac{2}{3}}\]

Method 2: Using joint density directly

\[E[Y_1] = \int_0^1 \int_0^1 y_1 \cdot 2y_1 \, dy_2 \, dy_1 = \int_0^1 2y_1^2 \left[ y_2 \right]_0^1 dy_1 = \frac{2}{3}\]

Both methods give the same answer!

🧮 Theorems on Expected Values

Theorems 5.6-5.8: Linearity of Expected Value

Theorem 5.6: \(E[c] = c\) for any constant \(c\)

Theorem 5.7: \(E[c \cdot g(Y_1, Y_2)] = c \cdot E[g(Y_1, Y_2)]\)

Theorem 5.8: \(E[g_1(Y_1, Y_2) + g_2(Y_1, Y_2)] = E[g_1(Y_1, Y_2)] + E[g_2(Y_1, Y_2)]\)

🌟 Corollary: Fundamental Result

\[\boxed{E[Y_1 + Y_2] = E[Y_1] + E[Y_2]}\]

This holds always, regardless of whether \(Y_1\) and \(Y_2\) are independent!

More generally: \(E[aY_1 + bY_2 + c] = aE[Y_1] + bE[Y_2] + c\)

📌 Example 3: Expected Portfolio Return

Problem: An investor holds a portfolio with weight \(w_1 = 0.6\) in Stock A (expected return 8%) and \(w_2 = 0.4\) in Stock B (expected return 12%). Find the expected portfolio return.

Let \(Y_1\) = return on Stock A, \(Y_2\) = return on Stock B.

Portfolio return: \(R_p = w_1 Y_1 + w_2 Y_2 = 0.6 Y_1 + 0.4 Y_2\)

By linearity of expected value:

\[E[R_p] = E[0.6 Y_1 + 0.4 Y_2] = 0.6 E[Y_1] + 0.4 E[Y_2]\]

\[= 0.6(0.08) + 0.4(0.12) = 0.048 + 0.048 = \boxed{0.096 = 9.6\%}\]

Key Point: Expected portfolio return is simply the weighted average of individual expected returns—no covariance needed!

🧮 Theorem 5.9: Independence and Expected Values

Theorem 5.9: Product of Independent Variables

If \(Y_1\) and \(Y_2\) are independent, then for any functions \(g\) and \(h\):

\[E[g(Y_1) \cdot h(Y_2)] = E[g(Y_1)] \cdot E[h(Y_2)]\]

Special Case: \[E[Y_1 \cdot Y_2] = E[Y_1] \cdot E[Y_2] \quad \text{(if independent)}\]

Warning

Warning: The converse is NOT true! \(E[Y_1 Y_2] = E[Y_1] E[Y_2]\) does not imply independence.

Tip

Verification (Example 1): We found \(E[Y_1 Y_2] = 1/3\) and \(E[Y_1] = 2/3\).

For independent case: We’d also need \(E[Y_2] = 1/2\) (uniform on \([0,1]\)).

Check: \(E[Y_1] \cdot E[Y_2] = (2/3)(1/2) = 1/3 = E[Y_1 Y_2]\) ✓

📖 Definition: Covariance

📝 Definition 5.10: Covariance

The covariance of two random variables \(Y_1\) and \(Y_2\) is:

\[\text{Cov}(Y_1, Y_2) = E[(Y_1 - \mu_1)(Y_2 - \mu_2)]\]

where \(\mu_1 = E[Y_1]\) and \(\mu_2 = E[Y_2]\).

Interpretation:

- Positive covariance: Variables tend to deviate from their means in the same direction

- Negative covariance: Variables tend to deviate in opposite directions

- Zero covariance: No linear relationship (but variables may still be dependent!)

Notation: \(\text{Cov}(Y_1, Y_2) = \sigma_{12}\) or \(\sigma_{Y_1 Y_2}\)

🧮 Theorem 5.10: Computational Formula for Covariance

Theorem 5.10: Shortcut Formula

\[\text{Cov}(Y_1, Y_2) = E[Y_1 Y_2] - \mu_1 \mu_2 = E[Y_1 Y_2] - E[Y_1] \cdot E[Y_2]\]

Proof: \[\text{Cov}(Y_1, Y_2) = E[(Y_1 - \mu_1)(Y_2 - \mu_2)]\] \[= E[Y_1 Y_2 - \mu_2 Y_1 - \mu_1 Y_2 + \mu_1 \mu_2]\] \[= E[Y_1 Y_2] - \mu_2 E[Y_1] - \mu_1 E[Y_2] + \mu_1 \mu_2\] \[= E[Y_1 Y_2] - \mu_1 \mu_2 - \mu_1 \mu_2 + \mu_1 \mu_2 = E[Y_1 Y_2] - \mu_1 \mu_2\]

Key Insight: If \(Y_1\) and \(Y_2\) are independent, then \(E[Y_1 Y_2] = E[Y_1] E[Y_2]\), so \(\text{Cov}(Y_1, Y_2) = 0\).

📌 Example 4: Computing Covariance

Problem: For the joint density from Example 1, \(f(y_1, y_2) = 2y_1\) on \([0,1] \times [0,1]\), find \(\text{Cov}(Y_1, Y_2)\).

Solution:

From previous examples:

- \(E[Y_1] = 2/3\)

- \(E[Y_2] = 1/2\) (uniform on \([0,1]\))

- \(E[Y_1 Y_2] = 1/3\)

Using the computational formula:

\[\text{Cov}(Y_1, Y_2) = E[Y_1 Y_2] - E[Y_1] \cdot E[Y_2]\] \[= \frac{1}{3} - \frac{2}{3} \cdot \frac{1}{2} = \frac{1}{3} - \frac{1}{3} = \boxed{0}\]

Interpretation: Zero covariance confirms independence (from Theorem 5.5). Stock returns have no linear relationship.

📖 Definition: Correlation Coefficient

📝 Definition 5.11: Correlation Coefficient

The correlation coefficient between \(Y_1\) and \(Y_2\) is:

\[\rho = \rho_{Y_1, Y_2} = \frac{\text{Cov}(Y_1, Y_2)}{\sigma_1 \sigma_2}\]

where \(\sigma_1 = \sqrt{V(Y_1)}\) and \(\sigma_2 = \sqrt{V(Y_2)}\) are the standard deviations.

🌟 Properties of Correlation

- Bounded: \(-1 \leq \rho \leq 1\) always

- Dimensionless: No units, unlike covariance

- Standardized: Same interpretation across different scales

- Perfect linear relationship: \(|\rho| = 1\) if and only if \(Y_2 = a + bY_1\) for constants \(a, b\)

📌 Correlation Interpretation Guide

Correlation Values:

- \(\rho = +1\): Perfect positive linear

- \(\rho > 0.7\): Strong positive

- \(0.3 < \rho < 0.7\): Moderate positive

- \(-0.3 < \rho < 0.3\): Weak/no correlation

- \(\rho < -0.7\): Strong negative

- \(\rho = -1\): Perfect negative linear

Financial Examples:

- Stocks in same sector: \(\rho \approx 0.6-0.8\)

- Stocks and bonds: \(\rho \approx -0.2\) to \(+0.2\)

- Gold and USD: \(\rho \approx -0.3\) to \(-0.5\)

- S&P 500 vs individual stocks: \(\rho \approx 0.4-0.9\)

🧮 Theorem 5.11: Variance of Linear Combinations

Theorem 5.11: Portfolio Variance Formula

For any constants \(a\) and \(b\):

\[V(aY_1 + bY_2) = a^2 V(Y_1) + b^2 V(Y_2) + 2ab \text{ Cov}(Y_1, Y_2)\]

In terms of correlation:

\[V(aY_1 + bY_2) = a^2 \sigma_1^2 + b^2 \sigma_2^2 + 2ab\rho\sigma_1\sigma_2\]

Special Cases:

- If \(Y_1\) and \(Y_2\) are independent: \(\rho = 0\), so \(V(aY_1 + bY_2) = a^2 V(Y_1) + b^2 V(Y_2)\)

- For a portfolio with weights \(w_1\) and \(w_2\): \[\sigma_p^2 = w_1^2\sigma_1^2 + w_2^2\sigma_2^2 + 2w_1w_2\rho\sigma_1\sigma_2\]

📌 Example 5: Portfolio Standard Deviation

Problem: Portfolio with \(w_1 = 0.6\) in Stock A (\(\sigma_1 = 20\%\)) and \(w_2 = 0.4\) in Stock B (\(\sigma_2 = 15\%\)), with correlation \(\rho = 0.5\). Find portfolio standard deviation.

Solution: Using the portfolio variance formula:

\[\sigma_p^2 = w_1^2\sigma_1^2 + w_2^2\sigma_2^2 + 2w_1w_2\rho\sigma_1\sigma_2\]

\[= (0.6)^2(0.20)^2 + (0.4)^2(0.15)^2 + 2(0.6)(0.4)(0.5)(0.20)(0.15)\]

\[= 0.0144 + 0.0036 + 0.0072 = 0.0252\]

\[\sigma_p = \sqrt{0.0252} = 0.1587 = \boxed{15.87\%}\]

Key Insight: Portfolio risk (15.87%) < weighted average of individual risks (18%) due to diversification!

🤝 Think-Pair-Share Activity

💭 Diversification Paradox

Scenario: You have two investment options:

Option A:

- 100% in Stock X (\(\mu = 10\%\), \(\sigma = 25\%\))

Option B:

- 50% Stock X + 50% Stock Y (\(\mu_Y = 8\%\), \(\sigma_Y = 20\%\), \(\rho = -0.3\))

Questions:

- Calculate expected return for both options

- Calculate standard deviation for both options

- Which option would you choose and why?

Activity: (3 minutes)

- 1 min: Think individually and calculate

- 1 min: Pair up and discuss your answers

- 1 min: Share key insights with class

🤝 Think-Pair-Share: Solutions

Expected Returns:

Option A:

\[E[R_A] = 10\%\]

Option B: \[E[R_B] = 0.5(10\%) + 0.5(8\%) = 9\%\]

Standard Deviations:

Option A:

\[\sigma_A = 25\%\]

Option B: \[\sigma_B^2 = (0.5)^2(0.25)^2 + (0.5)^2(0.20)^2\] \[+ 2(0.5)(0.5)(-0.3)(0.25)(0.20)\] \[= 0.015625 + 0.01 - 0.0075 = 0.018125\] \[\sigma_B = 13.46\%\]

Key Insight: Option B has lower return (9% vs 10%) but much lower risk (13.46% vs 25%)! The negative correlation provides powerful diversification. Most investors would prefer B for better risk-adjusted returns.

🎯 Minimum Variance Portfolio: The Optimization Problem

📝 Mathematical Formulation

Given:

- Two assets with standard deviations \(\sigma_1\) and \(\sigma_2\) (volatilities)

- Correlation coefficient \(\rho\) between the assets

- Portfolio weights: \(w_1\) and \(w_2\) where \(w_1 + w_2 = 1\)

Optimization Problem:

\[\min_{w_1, w_2} \quad \sigma_p^2 = w_1^2\sigma_1^2 + w_2^2\sigma_2^2 + 2w_1w_2\rho\sigma_1\sigma_2\]

\[\text{subject to:} \quad w_1 + w_2 = 1, \quad w_1, w_2 \geq 0 \text{ (no short selling)}\]

Solution (using calculus):

Substitute \(w_2 = 1 - w_1\), take derivative with respect to \(w_1\), and set to zero:

\[w_1^* = \frac{\sigma_2^2 - \rho\sigma_1\sigma_2}{\sigma_1^2 + \sigma_2^2 - 2\rho\sigma_1\sigma_2}, \quad w_2^* = 1 - w_1^*\]

Key Insight: Optimal weights depend on both variances and correlation!

📊 Interactive: Minimum Variance Portfolio vs Correlation

Code

viewof rho_slider = {

const input = Inputs.range([-1, 1], {

value: 0.3,

step: 0.1,

label: "Correlation (ρ):",

format: d => d.toFixed(2)

});

input.addEventListener('pointerdown', e => e.stopPropagation());

input.addEventListener('touchstart', e => e.stopPropagation());

input.addEventListener('mousedown', e => e.stopPropagation());

input.addEventListener('click', e => e.stopPropagation());

input.addEventListener('wheel', e => e.stopPropagation());

input.addEventListener('pointermove', e => e.stopPropagation());

input.addEventListener('touchmove', e => e.stopPropagation());

return input;

}Code

sigma1 = 0.20 // 20% volatility for Asset 1

sigma2 = 0.15 // 15% volatility for Asset 2

// Calculate optimal minimum variance portfolio weight

// w1* = (σ₂² - ρσ₁σ₂) / (σ₁² + σ₂² - 2ρσ₁σ₂)

w1_optimal = (Math.pow(sigma2, 2) - rho_slider * sigma1 * sigma2) /

(Math.pow(sigma1, 2) + Math.pow(sigma2, 2) - 2 * rho_slider * sigma1 * sigma2)

// Constrain to [0, 1] (no short selling)

w1_star = Math.max(0, Math.min(1, w1_optimal))

w2_star = 1 - w1_star

// Minimum variance portfolio statistics

min_var = Math.pow(w1_star * sigma1, 2) +

Math.pow(w2_star * sigma2, 2) +

2 * w1_star * w2_star * rho_slider * sigma1 * sigma2

min_std = Math.sqrt(min_var)

// Generate efficient frontier data

weights = d3.range(0, 1.01, 0.01)

frontier_data = weights.map(w1 => {

const w2 = 1 - w1;

const var_p = Math.pow(w1 * sigma1, 2) +

Math.pow(w2 * sigma2, 2) +

2 * w1 * w2 * rho_slider * sigma1 * sigma2;

return {

w1: w1,

std: Math.sqrt(var_p)

};

})Code

Plot.plot({

width: 820,

height: 460,

marginLeft: 60,

marginBottom: 40,

x: {

label: "Weight in Asset 1",

domain: [0, 1],

grid: true

},

y: {

label: "Portfolio Std Dev",

tickFormat: d => `${(d * 100).toFixed(1)}%`,

grid: true

},

marks: [

Plot.line(frontier_data, {

x: "w1",

y: "std",

stroke: "#2ecc71",

strokeWidth: 3

}),

// Minimum variance portfolio point

Plot.dot([{

x: w1_star,

y: min_std

}], {

x: "x",

y: "y",

r: 8,

fill: "#e74c3c",

stroke: "#c0392b",

strokeWidth: 2

}),

// Individual assets

Plot.dot([

{x: 0, y: sigma2, label: "Asset 2"},

{x: 1, y: sigma1, label: "Asset 1"}

], {

x: "x",

y: "y",

r: 5,

fill: "#3498db"

}),

Plot.text([

{x: 0.05, y: sigma2, label: "Asset 2", dx: 15},

{x: 0.95, y: sigma1, label: "Asset 1", dx: 15}

], {

x: "x",

y: "y",

text: "label",

dx: "dx",

fontSize: 12,

fontWeight: "bold"

}),

// Label for minimum variance portfolio

Plot.text([{

x: w1_star,

y: min_std+0.005,

label: "Min Variance",

dy: -20

}], {

x: "x",

y: "y",

text: "label",

dy: "dy",

fontSize: 11,

fontWeight: "bold",

fill: "#e74c3c"

})

]

})Code

html`<div style="text-align: center; font-size: 1.1em; margin-top: 10px;">

<strong>Minimum Variance Portfolio:</strong> w₁* = ${(w1_star * 100).toFixed(1)}%,

w₂* = ${(w2_star * 100).toFixed(1)}% |

σₚ = ${(min_std * 100).toFixed(2)}% |

ρ = ${rho_slider.toFixed(2)}<br>

<em style="font-size: 0.9em;">Optimal weights change with correlation! Lower ρ → greater diversification benefit</em>

</div>`💰 Case Study: Real Portfolio Data

Using real data from 2010-2024:

- SPY (S&P 500 ETF): Large-cap US stocks

- TLT (20+ Year Treasury Bond ETF): Long-term government bonds

- GLD (Gold ETF): Precious metals

Code

library(tidyquant)

library(tidyverse)

library(knitr)

# Download monthly returns

symbols <- c("SPY", "TLT", "GLD")

prices <- tq_get(symbols,

from = "2010-01-01",

to = "2024-12-31",

get = "stock.prices")

# Calculate monthly returns

returns <- prices %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "return")

# Convert to matrix format

returns_matrix <- returns %>%

pivot_wider(names_from = symbol, values_from = return) %>%

select(-date) %>%

as.matrix()

# Compute statistics

cov_matrix <- cov(returns_matrix) * 12 # Annualize

cor_matrix <- cor(returns_matrix)

# Summary statistics

summary_stats <- data.frame(

Asset = symbols,

Mean = colMeans(returns_matrix) * 12 * 100, # Annualized %

StdDev = apply(returns_matrix, 2, sd) * sqrt(12) * 100, # Annualized %

Sharpe = (colMeans(returns_matrix) * 12) / (apply(returns_matrix, 2, sd) * sqrt(12))

)

kable(summary_stats, digits = 2,

caption = "Asset Statistics (2010-2024, Annualized)")| Asset | Mean | StdDev | Sharpe | |

|---|---|---|---|---|

| SPY | SPY | 13.95 | 14.59 | 0.96 |

| TLT | TLT | 3.57 | 13.89 | 0.26 |

| GLD | GLD | 6.45 | 15.62 | 0.41 |

💰 Case Study: Correlation Matrix

📊 Key Observations

- SPY-TLT: Low/slightly negative correlation → good diversification

- SPY-GLD: Low positive correlation → some diversification benefit

- TLT-GLD: Moderate positive correlation → less diversification between these two

Investment Implication: Combining stocks (SPY) with bonds (TLT) provides excellent risk reduction due to low correlation.

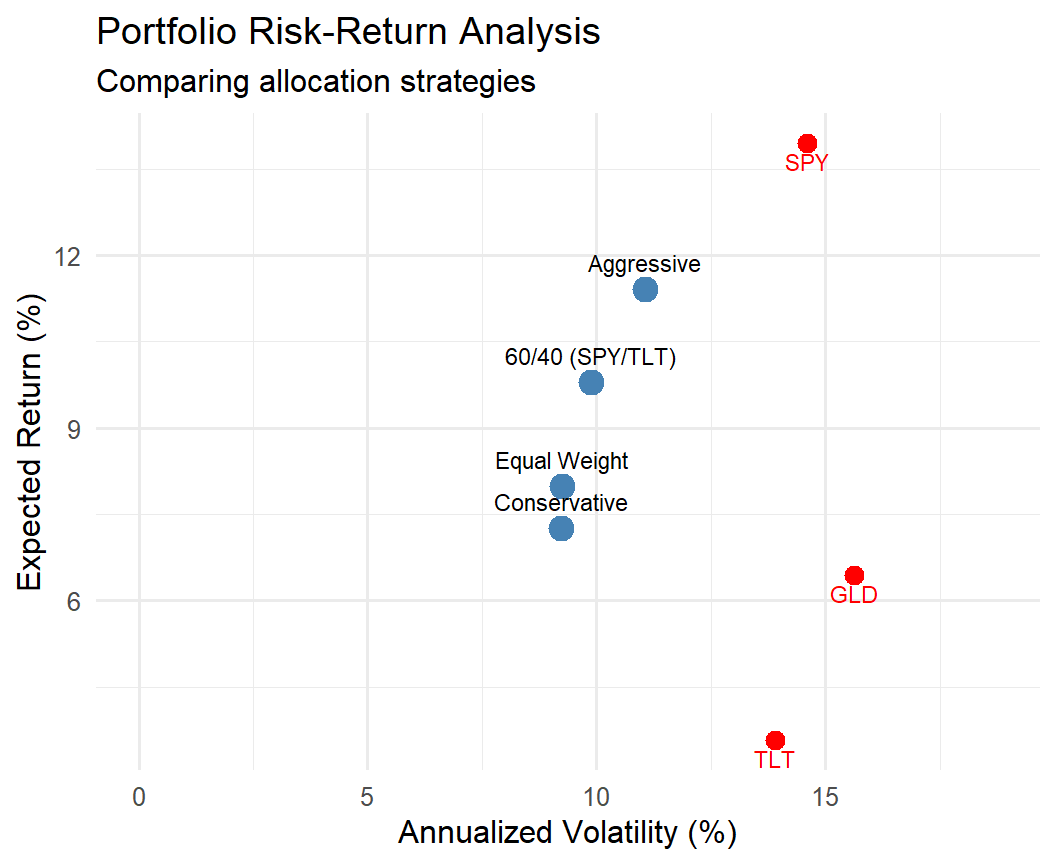

💰 Case Study: Portfolio Analysis

Code

# Define different portfolio allocations

portfolios <- list(

"Equal Weight" = c(1/3, 1/3, 1/3),

"60/40 (SPY/TLT)" = c(0.6, 0.4, 0.0),

"Conservative" = c(0.3, 0.5, 0.2),

"Aggressive" = c(0.7, 0.1, 0.2)

)

# Expected returns (annualized)

mu <- colMeans(returns_matrix) * 12

# Portfolio metrics

results <- data.frame(

Portfolio = character(),

ExpReturn = numeric(),

StdDev = numeric(),

Sharpe = numeric()

)

for(name in names(portfolios)) {

w <- portfolios[[name]]

port_return <- sum(w * mu)

port_var <- t(w) %*% cov_matrix %*% w

port_std <- sqrt(port_var)

sharpe <- port_return / port_std

results <- rbind(results, data.frame(

Portfolio = name,

ExpReturn = port_return * 100,

StdDev = port_std * 100,

Sharpe = sharpe

))

}

kable(results, digits = 2, row.names = FALSE)| Portfolio | ExpReturn | StdDev | Sharpe |

|---|---|---|---|

| Equal Weight | 7.99 | 9.25 | 0.86 |

| 60/40 (SPY/TLT) | 9.79 | 9.89 | 0.99 |

| Conservative | 7.26 | 9.24 | 0.79 |

| Aggressive | 11.41 | 11.05 | 1.03 |

Code

library(ggplot2)

# Plot portfolios on risk-return space

ggplot(results, aes(x = StdDev, y = ExpReturn)) +

geom_point(size = 4, color = "steelblue") +

geom_text(aes(label = Portfolio),

vjust = -1, hjust = 0.5, size = 3) +

geom_point(data = data.frame(

StdDev = summary_stats$StdDev,

ExpReturn = summary_stats$Mean

), color = "red", size = 3) +

geom_text(data = data.frame(

StdDev = summary_stats$StdDev,

ExpReturn = summary_stats$Mean,

label = c("SPY", "TLT", "GLD")

), aes(label = label), vjust = 1.5,

color = "red", size = 3) +

labs(title = "Portfolio Risk-Return Analysis",

subtitle = "Comparing allocation strategies",

x = "Annualized Volatility (%)",

y = "Expected Return (%)") +

theme_minimal(base_size = 12) +

xlim(0, max(summary_stats$StdDev) * 1.2)

💰 Case Study: Key Findings

📊 Analysis Results

Correlation Insights:

SPY-TLT: Low/negative → good diversification

SPY-GLD: Low positive → some benefit

TLT-GLD: Moderate positive

Low correlations reduce risk

Portfolio Variance:

Equal-weight portfolio has lower risk:

\[\sigma_p^2 = \sum_i w_i^2 \sigma_i^2 \] \[+2\sum_{i<j} w_i w_j \rho_{ij} \sigma_i \sigma_j\]

Low/negative ρ reduces variance!

Investment Implications:

Diversification works

Correlation matters most

Trade-off: lower risk = lower return

📝 Quiz #1: Computing Expected Value

If \(E[Y_1] = 5\), \(E[Y_2] = 10\), what is \(E[3Y_1 + 2Y_2 - 7]\)?

- 28

- 35

- 22

- 15

📝 Quiz #2: Covariance Computation

If \(E[Y_1] = 2\), \(E[Y_2] = 3\), and \(E[Y_1 Y_2] = 7\), what is \(\text{Cov}(Y_1, Y_2)\)?

- 1

- 6

- 7

- -1

📝 Quiz #3: Independence and Covariance

Which statement about covariance is TRUE?

- If two variables are independent, their covariance must be zero

- If covariance is zero, the variables must be independent

- Covariance can be greater than 1

- Covariance equals correlation divided by the product of standard deviations

📝 Quiz #4: Portfolio Variance

For a portfolio with \(w_1 = w_2 = 0.5\), \(\sigma_1 = \sigma_2 = 20\%\), and \(\rho = 0\), what is the portfolio standard deviation?

- 14.14%

- 20%

- 10%

- 28.28%

📝 Summary

✅ Key Takeaways

Expected value of functions \(E[g(Y_1, Y_2)]\) is computed by weighting function values by joint probabilities/densities

Linearity: \(E[aY_1 + bY_2] = aE[Y_1] + bE[Y_2]\) always holds; \(E[Y_1 Y_2] = E[Y_1]E[Y_2]\) only if independent

Covariance \(\text{Cov}(Y_1, Y_2) = E[Y_1 Y_2] - E[Y_1]E[Y_2]\) measures linear association

Correlation \(\rho = \text{Cov}(Y_1, Y_2)/(\sigma_1 \sigma_2)\) is standardized with \(-1 \leq \rho \leq 1\)

Critical insight: \(\text{Cov} = 0\) does NOT imply independence!

Portfolio variance: \(V(w_1 Y_1 + w_2 Y_2) = w_1^2 V(Y_1) + w_2^2 V(Y_2) + 2w_1 w_2 \text{Cov}(Y_1, Y_2)\)

📚 Practice Problems

📝 Homework Problems

Problem 1: For \(f(y_1, y_2) = 8y_1y_2\) on \(0 < y_1 < 1\), \(0 < y_2 < 1\), find \(E[Y_1 + Y_2]\) and \(E[Y_1 Y_2]\).

Problem 2: For \(f(y_1, y_2) = 2\) on \(0 < y_1 < 1\), \(0 < y_2 < y_1\), compute \(\text{Cov}(Y_1, Y_2)\).

Problem 3: Two stocks: \(\sigma_1 = 30\%\), \(\sigma_2 = 20\%\), \(\text{Cov} = 0.024\). Find correlation.

Problem 4: Portfolio: \(w_1 = 0.4\), \(w_2 = 0.6\), \(\mu_1 = 12\%\), \(\mu_2 = 8\%\), \(\sigma_1 = 25\%\), \(\sigma_2 = 15\%\), \(\rho = 0.3\). Find expected return and standard deviation.

Problem 5: Verify for \(Y_1 \sim \text{Uniform}(-1, 1)\) and \(Y_2 = Y_1^2\): \(\text{Cov}(Y_1, Y_2) = 0\) but variables are dependent.

📱 Late Check-in

👋 Thank You!

📬 Contact Information:

Samir Orujov, PhD

Assistant Professor

School of Business

ADA University

📧 Email: sorujov@ada.edu.az

🏢 Office: D312

⏰ Office Hours: By appointment

📅 Next Class:

Topic: Functions of Random Variables (Chapter 6)

Reading: Chapter 6, Sections 6.1-6.3

Preparation: Review change of variables in calculus

⏰ Reminders:

✅ Complete Practice Problems 1-5

✅ Master the portfolio variance formula

✅ Remember: Cov = 0 ≠ independence!

✅ Work hard!

❓ Questions?

💬 Open Discussion

Key Topics for Discussion:

Why is covariance so important in finance and portfolio theory?

Can you think of examples where two variables have zero covariance but are clearly dependent?

How would you estimate covariance from sample data? What are the challenges?

What happens to diversification benefits during financial crises when correlations spike?

Mathematical Statistics - Covariance and Correlation