Problem 1 (Transformation – Risk): An insurance loss is modeled as \(Y \sim \text{Exponential}(2)\). Use the transformation method to find the pdf of the cube-root loss severity \(U = Y^{1/3}\).

Problem 2 (Log-Normal – Stock Pricing): A stock price follows \(S \sim \text{LogNormal}(4, 0.09)\). Find \(E[S]\) and \(P(S > 60)\).

Problem 3 (MGF – Claim Counts): Two branch offices have independent claim counts \(Y_1 \sim \text{Poisson}(\lambda_1)\) and \(Y_2 \sim \text{Poisson}(\lambda_2)\). Use MGFs to show total claims \(Y_1 + Y_2 \sim \text{Poisson}(\lambda_1 + \lambda_2)\).

Problem 4 (Chi-Square – Variance Test): A risk analyst standardizes 10 independent daily returns to get \(Z_i \sim N(0,1)\). Find \(P(\sum Z_i^2 > 18.31)\) to test if realized variance is unexpectedly high.

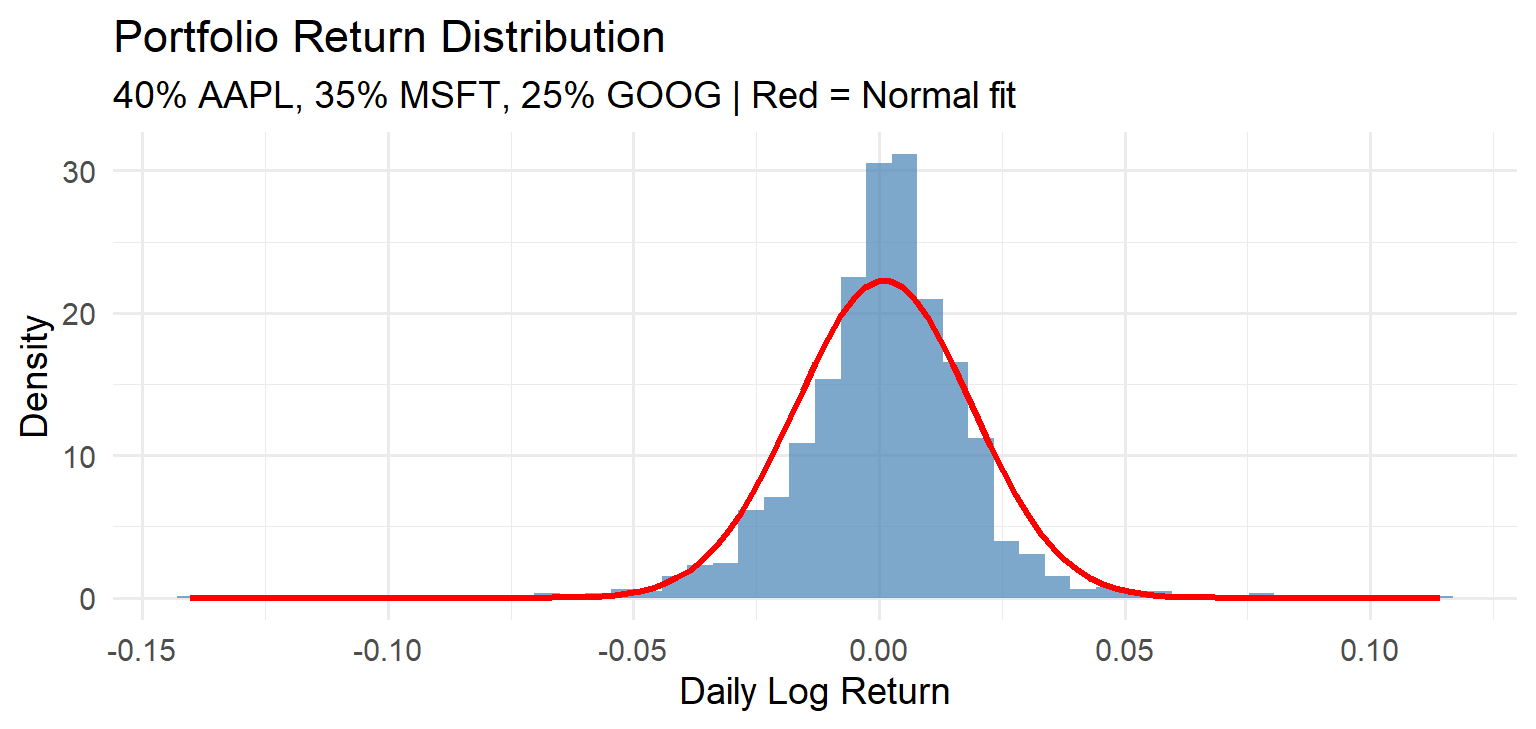

Problem 5 (Portfolio): A pension fund holds two uncorrelated asset classes with returns \(N(0.08, 0.04)\) and \(N(0.05, 0.01)\). Find the distribution of the 60-40 portfolio return using the MGF method.